FOR ADDITIONAL INFORMATION, CLICK HERE!

February/2015

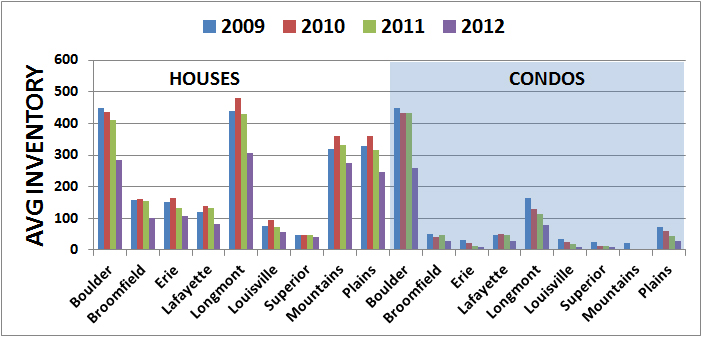

At the end of December/2011, there were 1,121 single-family home listings available for sale across Boulder County. That number shrank to 814 at the end of December/2012; 679 at the end of December/2013; and 678 at the end of December/2014. Thus we begin our fourth year of a listing drought in Boulder County.

There are pluses and minuses to the impact of a reduction in available housing inventory. On the plus side, scarcity creates demand, which in turn results in an increase in home values. Builders sense buyer pent-up demand and churn up ground for new homes, characterized by small lots and populated by pocket parks strewn throughout the subdivision. On the minus side, buyers often find themselves in a position where they can neither dictate a strong negotiating position nor dally in making a decision, as other buyers may come swooping in. To the victor belong the spoils, with the spoils meaning goods or benefit taken from the loser in a competitive situation.

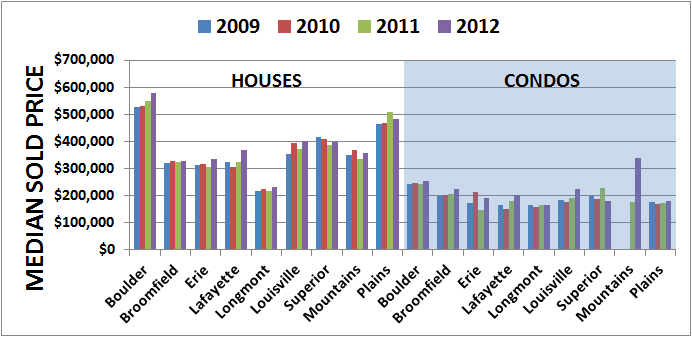

From a pricing perspective, homes at an entry to mid-range price point sell the quickest, simply because there are more buyers in those price ranges. These buyers occupy three different levels of interest: (1) Entry Level (first-time buyers); (2) Move Up (buyers who need more room; normally due to a growing family); (3) Move Down (buyers who need less space; normally due to a dwindling family; the empty nester syndrome).

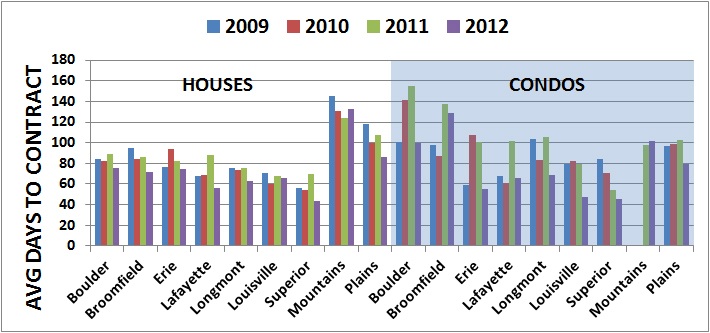

As the housing price point increases, the number of prospective buyers decreases. For Boulder County, an example of this is homes priced at a million dollars and up. At the end of December/2014 there were 141 active single family home listings on the market for sale priced at a million dollars and up. There were 245 single family homes sold in Boulder County in 2014 priced at a million dollars and up. That resulted in an Absorption Rate of approximately 149 days or slightly less than five months. The Absorption Rate in 2014 for homes priced under a million dollars in Boulder County was 65 days. (In January/2015 there were nine single family home sales priced at a million dollars and up. There are 141 active single family home listings in that price range. The resulting Absorption Rate is 554 days.)

2015 promises to look a lot like 2014. Available inventory for Boulder County will continue to expand as the waning days of winter give way to spring. At the end of January/2015 there were 700 active single family homes for sale in Boulder County; up slightly from the 678 active listings at the end of 2014.

Home values will continue to increase, but are projected to rise more slowly. According to Forbes, nationally prices are near their spring 2005 levels. For Boulder County, 2005 was when the real estate market peaked. There were 4,193 single family home sales in 2005 (3,251 single family home sales in 2014) and 1,602 attached unit sales in 2005 (1,391 attached unit sales in 2014).

New home construction continues to flourish across east Boulder County - Erie in particular, with in-fill construction going on in Boulder and pocket areas of Superior, Louisville, and Lafayette. Despite the increase in overall inventory, the vacancy rate for rental properties in Boulder County is around 3.3% (Apartment Association of Metro Denver). Look for rental rates to continue to increase in 2015.