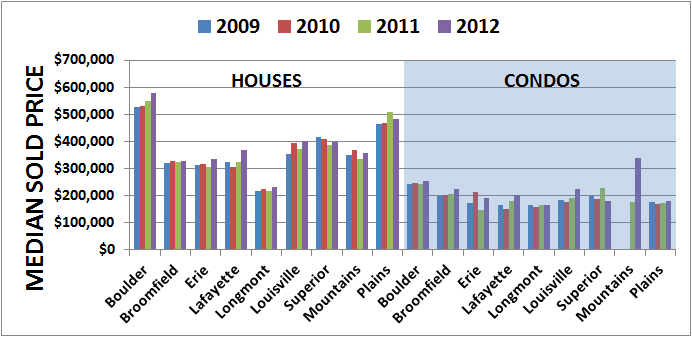

Pleased to announce the successful sale of 809 Bass Circle in the Lafayette Park Neighborhood of Lafayette. I was a buyer's agent representing a sweet first-time home buying couple due to get married later this summer. So they will be starting their lives together in this nice little 3bd/2ba ~1,300 sq ft house w/1 car garage and a nicely landscaped 8,100 sq ft lot. Purchase price was $232,000 with $2,000 in closing costs credit.

{kind=link}